Knowing your net worth is an important tool when trying to improve your financial situation. Like how companies monitor and report on their net worth, individuals can do the same. Your net worth is the amount left over after you deduct your liabilities (what you owe) from your assets (what you own) at a point in time. Tracking this value and the changes over time can keep you on track to meet your financial goals.

Why track net worth?

Keeping a running tally of your net worth can help you achieve your financial goals. If you’re saving for a car, house or your general financial future, seeing the figures on paper (or in Excel) can keep you on track to continue saving. If you’re trying to reduce your credit card debt, tracking your net worth can show you your progress and help you stick to a plan.

Tracking your net worth can be likened to that of weighing yourself. When you’re trying to lose weight, your measurement tool is generally a scale. When you weigh in and see the number on the scale decrease, you can see your progress and the fruits of your efforts working. Similarly, when you’re trying to improve your financial situation, monitoring your net worth can help you to see your progress. If you do this regularly, you will see the picture change over time and be more mindful financially.

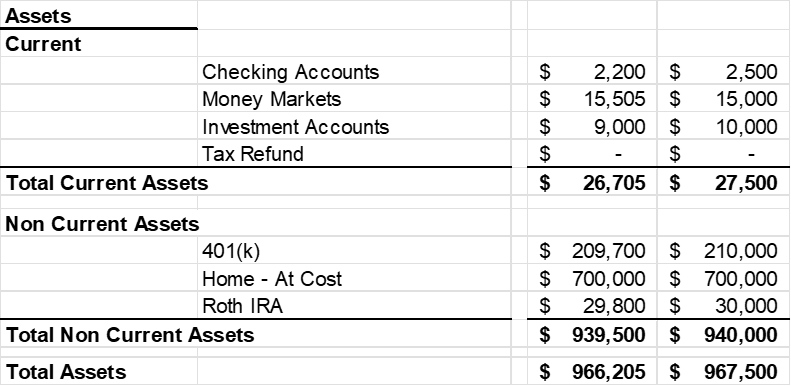

Assets

Assets, in the simplest of definitions, include anything that consists of cash or can be turned into cash in the future. Some examples of assets include bank balances and investments including your house, your car, or your retirement savings.

When tracking your net worth, it’s helpful to classify your assets as current or non-current assets. Doing so helps you know how much liquidity you have should you need access to funds in the near term. Current assets are those that can be cashed in immediately (or generally within 1 year). Non-current assets are those that you don’t expect to cash in for over a year. Here’s how your assets might look on a statement of net worth:

As shown in the example above, included in current assets are funds available in your checking account, money markets and investment accounts that are general investments and not related to retirement. The long term assets are those that you can’t easily turn into cash in the immediate future. The examples of 401k and Roth IRA are classified above as long term if you aren’t at retirement age. The home value of your residence is also generally considered long term as you probably don’t expect to sell in the near term.

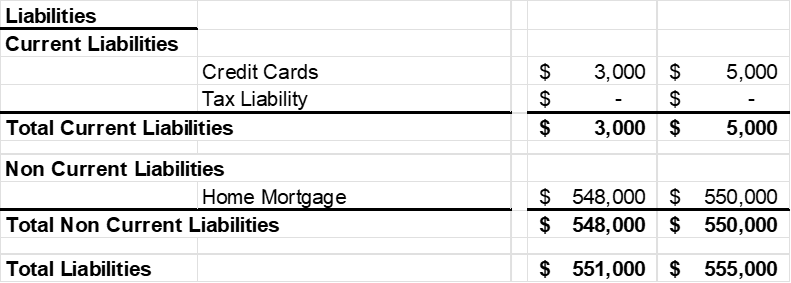

Liabilities

Liabilities are those amounts you owe to others. Some examples of this include credit card debt, loans including mortgages, and tax liabilities. It’s helpful to track current vs non-current liabilities in the same way as assets. This shows how much of your liabilities are due in the short term. Here’s how your liabilities section of a statement of net worth may look:

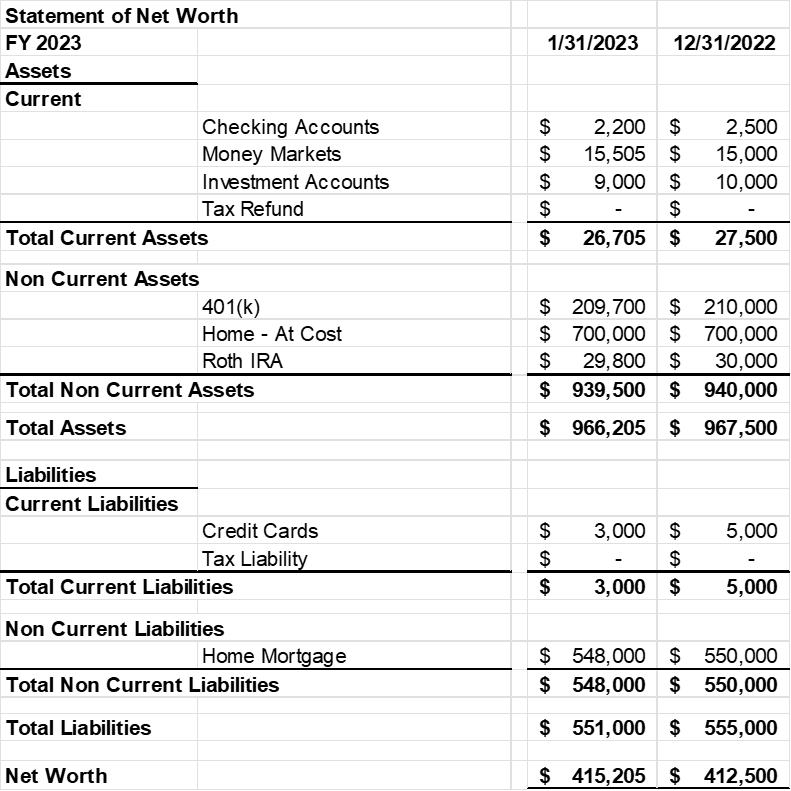

Net Worth

And the moment we’ve been waiting for! Your net worth is your financial position after measuring all assets and deducting all liabilities at a point in time. This is what you are worth (at least financially!) A positive net worth means you have more assets to cover the amounts you owe. A negative net worth indicates you owe more than you have assets to cover them. Here’s a sample net worth statement using the same data we covered in previous sections.

What is this information telling us?

First and foremost, the net worth is a positive number meaning there are more assets than liabilities and if everything could be cashed in dollar for dollar, all liabilities would be able to be covered. (Note: If under retirement age, generally you can’t cash in 401ks or IRAs dollar for dollar as there may be penalty or other tax implications).

Second, the amount of current assets is well above the amount of current liabilities. This means that meeting financial obligations in the near term shouldn’t be a problem.

Third, the net worth amount is growing. At the end of December 2022, the net worth was $412,500. Now, at the end of January 2023, it’s $415,205. The amount of assets over liabilities in one month increased $2,705. This shows progress in increasing net worth and potentially on track to meet financial goals.

How often should I track my net worth?

Your net worth can be tracked with whatever frequency you choose. Although, daily tracking may be a bit much. If you track your net worth at least monthly, you can pick up on changes that may impact you reaching your goals and can change habits accordingly. You could also track your net worth weekly or bi-weekly, or whatever pay schedule you’re on. This could help prevent ups and downs between paychecks. The key is to track it regularly.

Final thoughts

Whatever your financial goals, tracking your net worth regularly will help you see your progress. By doing so at least monthly, you can catch any slip ups in your strategy to improve your financial situation and adjust accordingly. The exercise of tracking your net worth doesn’t take long to do but can be a useful tool to see you achieve your financial goals.

Disclaimer: The information contained in this post is general in nature and does not take into account your personal objectives, financial situation or needs. Therefore, you should consider whether the information is appropriate to your circumstances before acting on it, and where appropriate, seek professional advice from a finance professional.